Takeaways

- NSRF positions Malaysia to adopt global sustainability standards (IFRS S1 & S2), bringing clarity and rigour to ESG disclosures.

- The phased rollout (2025–2030) allows companies to scale maturity, but early movers will gain strategic advantage.

- Scope 3 emissions and external assurance are the toughest hurdles. Those who prepare ahead will mitigate compliance risks.

- Organisations that embed NSRF readiness into their core strategy will build long-term stakeholder trust, investor confidence, and operational resilience.

With global capital increasingly flowing to sustainable businesses, regulators are tightening disclosure rules worldwide. Malaysia’s NSRF represents a strategic leap, institutionalising sustainability disclosures in line with global norms.

For local and regional companies, the NSRF is more than a regulatory requirement. It is a market differentiator. Those who act early can lead in transparency, build investor trust, and embed climate resilience into their core operations.

Table of Contents

What is Malaysia’s National Sustainability Reporting Framework (NSRF)

Launched on 24 September 2024, the National Sustainability Reporting Framework (NSRF) sets Malaysia’s corporate sustainability reporting on a path aligned with IFRS Sustainability Disclosure Standards (ISSB). It leverages IFRS S1 (General Requirements) and IFRS S2 (Climate Disclosures) as its foundational pillars.

By standardising sustainability disclosures, NSRF helps ensure that sustainability data is consistent, comparable and credible. It is a key step toward market confidence and regulatory trust.

Why it matters

With global capital increasingly flowing to sustainable businesses, regulators are tightening disclosure rules worldwide. Malaysia’s NSRF is a strategic leap to institutionalise sustainability disclosures in tandem with global norms.

For local and regional companies, NSRF is more than a regulatory requirement. It’s a market differentiator: those who act early can lead in transparency, secure investor trust, and embed climate resilience into their DNA.

Who Needs to Comply and When

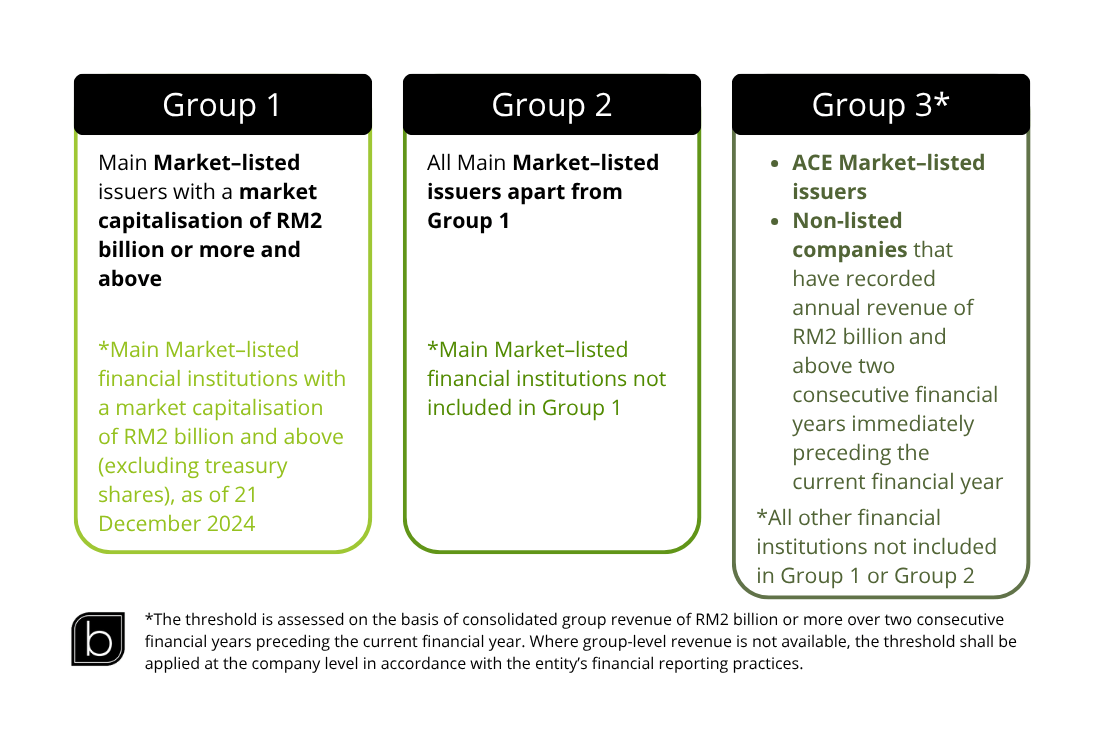

NSRF divides entities into three groups:

- Group 1:Main Market–listed issuers with a market capitalisation of RM2 billion or more and above.

- Group 2: All Main Market–listed issuers apart from Group 1.

- Group 3: ACE Market-listed firms and large non-listed firms with annual revenue of RM2 billion and above two consecutive financial years.

Implementation Timeline

What Disclosures Must Be Made

Under NSRF’s adoption of IFRS S1 and S2, organisations must disclose across these areas:

Governance: Board oversight and roles

Strategy & Business Model: How sustainability affects and is affected by operations

Risk Management: Identification and mitigation of sustainability risks

Metrics & Targets: Quantitative KPIs and emissions (Scope 1, 2, eventually 3)

Climate Disclosures: Climate-related scenario analysis, resilience, transition strategy

All disclosures must follow the principle of financial materiality: only those matters likely to influence investor decisions are required.

Transition Reliefs and Flexibility

To ease adoption, NSRF offers:

- Delayed Scope 3 reporting for certain groups in early years

- Segment-based disclosures, allowing focus on material business lines

- Exemptions for non-listed entities under parent firms already reporting under equivalent standards

- Proportional reporting—smaller entities may start with simplified disclosures

These mechanisms ensure NSRF is more accessible, not burdensome.

Assurance and Credibility

Mandatory external assurance is central to NSRF’s credibility.

- Reasonable assurance will be required initially for Scope 1 & 2 disclosures by Group 1 (by 2027).

- Assurance providers must adhere to recognised professional standards, ensuring sustainability data is reliable and not merely aspirational.

This move is intended to counter greenwashing and align sustainability data with the rigour applied to financial reporting.

How Businesses Should Prepare

We often see companies diving into NSRF readiness with quick fixes or template-driven reports. It feels like progress, but without a solid foundation, the effort usually leads to patchy results, inconsistent data, and lost opportunities.

Here is the Strategic Action Plan that companies can follow to embed NSRF into their core business strategies and operations:

- Gap Assessment

Benchmark your current ESG practices against IFRS S1 and IFRS S2 requirements. This reveals weaknesses in governance, risk management, and disclosure quality. Without this baseline, companies cannot prioritise improvements or demonstrate readiness. - Materiality Assessment

Identify the sustainability themes most relevant to your business and stakeholders. This ensures focus on the issues that drive financial impact, regulatory relevance, and investor interest. Skipping this step often results in reporting on everything and nothing at the same time. - Data Architecture

Build reliable systems to capture emissions, non-financial metrics, and assurance-ready datasets. Strong data architecture reduces errors, improves comparability, and makes reporting scalable across operations and value chains. Poor systems, in contrast, create inefficiencies and compliance risks. - Target and Scenario Analysis and Development

Set measurable, science-based targets and conduct climate-related scenario analysis. By modelling different climate futures, companies can stress-test their strategies and prepare for regulatory, market, and environmental shocks. Without this forward-looking planning, businesses risk being caught off guard. - Narrative Crafting

Translate technical disclosures into a clear story linking sustainability performance to financial outcomes. A strong narrative engages investors, builds trust, and positions the company as a responsible leader. Weak narratives leave reports unread and strategies misunderstood. - Assurance Planning

Engage assurance providers early to ensure data systems meet audit requirements. Waiting until the last minute leads to costly adjustments and audit failures. Early planning builds confidence and credibility in sustainability disclosures. - Capability Building

Invest in training, culture, and tools such as a ESG Software. Without capability building, companies risk treating NSRF as a compliance exercise rather than an opportunity for strategic transformation.

Besides, leadership involvement, cross-departmental alignment, and early investment are critical success factors. Strong board oversight, collaboration between finance, sustainability, and operations, and a proactive mindset will determine whether NSRF adoption is seen as a compliance burden or a competitive advantage.

At Bernard Business Consulting, we specialise in helping businesses in Malaysia and beyond integrate sustainability into their core strategies. With expertise in greenhouse gas management, ESG reporting, and climate compliance, we support organisations to accelerate their transition to net-zero while creating long-term value. Our practical solutions and targeted training empower companies to navigate evolving frameworks like NSRF and IFRS S2 with confidence and impact.

Join us at the International Greentech & Eco Products Exhibition and Conference Malaysia (IGEM) 2025, taking place from 15–17 October 2025 at the KLCC Convention Centre. We are providing a comprehensive NSRF readiness assessment, roadmap, and e-book designed to help businesses achieve NSRF compliance and manage GHG emissions more effectively.

In the lead-up to IGEM 2025, we are also hosting an exclusive webinar on “Understanding the National Sustainability Reporting Framework (NSRF)” to support your learning journey and ensure your organisation stays ahead of regulatory requirements. Learn more and register now.

Webinar

October 9, 2025 @ 2:00 PM to 2:30 PM MYT

Understanding Malaysia’s National Sustainability Reporting Framework

Gain practical insights into Malaysia’s National Sustainability Reporting Framework (NSRF), its links to IFRS S1 & S2, and actionable steps for compliance, governance, and value creation.